Procter & Gamble Co: One Dividend Stock for the Next 100 Years

What do General Mills, Inc. (NYSE:GIS), Exxon Mobil Corporation (NYSE:XOM), and Stanley Black & Decker, Inc. (NYSE:SWK) all have in common?

Simply put, all of these companies have soldiered through some of the biggest economic catastrophes of the past century. Hundreds of thousands of businesses have come and gone since the late 1800s. Yet through more than 100 years of political and economic upheaval, these three companies, and a handful of others like them, have managed to prosper.

Long-time subscribers know I have nicknamed this group of dividend stocks my “Forever Assets.” This elite collection of businesses has rewarded their shareholders, not just for years and decades, but for generations. And their unique competitive advantages have allowed them to consistently beat the market decade after decade.

Case in point this month: Procter & Gamble Co (NYSE:PG).

Admittedly, the consumer products giant doesn’t make for the most stimulating conversation around the office water cooler. But P&G has paid dividends for over a century. And, in recent years, shares have quietly produced returns comparable to most tech stocks.

P&G can trace its roots back to the 1830s. The founders, William Procter and James Gamble, started a successful business selling soap and candles in the frontier town of Cincinnati. But the company didn’t hit the big time until the Civil War, when P&G secured contracts to produce cleaning supplies to the Union army. (Source: “Heritage,” Procter & Gamble Co, last accessed August 18, 2020.)

Over the following decades,Procter & Gamble Co quietly assembled a consumer products empire. Today, the company owns dozens of top brands, including “Bounty” (paper towels), “Crest” (toothpaste), “Gillette” (razors), and “Tide” (laundry detergent). Altogether, this collection of cash cow businesses generates more than $70.1 billion in annual revenues. (Source: “The Procter & Gamble Company (PG) > Financials, Income Statement,” Yahoo! Finance, last accessed August 18, 2020.)

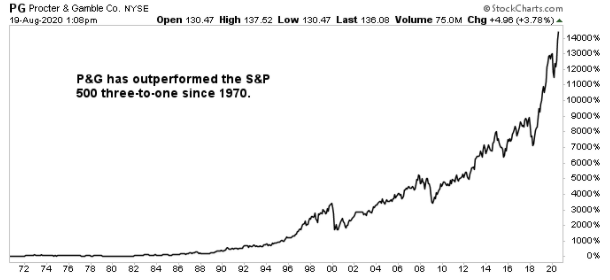

Chart courtesy of StockCharts.com

It’s not difficult to explain how P&G has survived while others failed.

Tech companies run on an endless innovation treadmill, spending billions on research and development each year. Sure, it makes for exciting coverage in the business press. But most of the products that come out of this investment are useless in a few years (just look at the “high-tech” “BlackBerry” smartphone sitting in your junk drawer). And if a business fails to lead the pace of innovation, it falls to the wayside in just a few years.

“Forever Assets” like P&G, however, don’t face this problem. For most of these companies, their core product has remained virtually the same for decades. And, in the case of P&G’s original brand, “Ivory” soap, management hasn’t changed the formula in almost a century. This allows the company to keep chugging along, cranking out respectable profits year after year and paying out dividends to shareholders.

Having such a long track record offers other advantages, too. Retailers, by and large, prefer to grant their best shelf spaces to proven suppliers over new startups. And over a century of marketing distinguishes P&G’s brands in store aisles.

So, while you and I could create a knockoff product, it would be difficult to replicate P&G’s relationships with vendors and customers overnight. This edge, which only comes after more than a century in business, allows management to earn above-average margins on every item it sells.

To see these competitive advantages in action, take a look at the firm’s return on equity (ROE). This number measures a business’ profit relative to the amount of capital shareholders have invested into the business.

In the case of Procter & Gamble Co, the company’s ROE topped 27.8% in 2019. And this wasn’t a one-off, either. Since 2014, the company’s ROE has consistently averaged around 17% per year. For comparison, the average ROE of a company in the S&P 500 is usually between 10% and 12% annually.

Of course, the real test of any “Forever Asset” is how well the business fares during a crisis. But through the COVID-19 pandemic, P&G has held up relatively well.

The company’s fourth-quarter financial results beat analysts’ expectations on both the top and bottom line. Overall, P&G saw a six-percent increase in total organic sales, which strips out the impact of acquisitions and divestments, blowing Wall Street’s projections out of the water. (Source: “P&G Announces Fourth Quarter and Fiscal Year 2020 Results,” Procter & Gamble Co, July 30, 2020.)

“We expect to grow through this crisis and come out even stronger on the other side,” P&G chairman and chief executive, David Taylor, wrote in a note to shareholders.

“We delivered strong, balanced sales and profit results in fiscal 2020, both pre-COVID and through the balance of the year, meeting or exceeding each of our going-in targets, demonstrating the commitment and agility of P&G people and the robustness of our strategy.” (Source: “P&G Announces Fourth Quarter and Fiscal Year 2020 Results,” Procter & Gamble Co, July 30, 2020.)

So, what does management do with the globs of cash flow that pile up in the business each year? For the most part, they pay it out to shareholders.

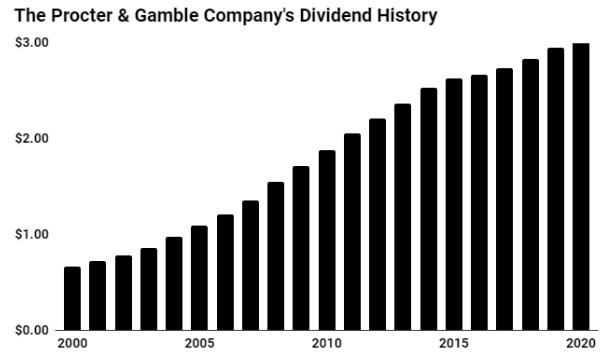

Earlier this year, executives boosted the company’s quarterly dividend by six percent to $0.79 per share. The move represents the company’s 63rd consecutive annual dividend increase and pads the stock’s lead as one of the longest-standing members in the list of “Dividend Aristocrats,” an elite group of companies that have raised their dividends for 25 straight years. (Source: The Procter & Gamble Company > Splits & Dividend History,” Procter & Gamble Co, last accessed August 19, 2020.)

Management also returns mountains of cash through the company’s share buyback program. Since 2017, executives have repurchased a total of $24.6 billion in stock, reducing the total number of outstanding shares by almost 10%.

In effect, this amounts to a “stealth dividend.” By quietly buying out fellow shareholders, loyal investors can increase their stake in a wonderful business tax-free. (Source: “The Procter & Gamble Company (PG) > Financials > Cash Flow,” Yahoo! Finance, last accessed August 19, 2020.)

Source: Procter & Gamble Co Investor Relations

So, with a pristine dividend track record, what could go wrong for P&G?

I see three big risks: higher costs, a looming recession, and a strong U.S. dollar.

Higher input costs present the biggest challenge. Across the consumer staples sector, the rising price of transportation and packaging materials has taken a bite out of margins. While P&G can offset these expenses over the long haul, higher costs could knock the share price from quarter to quarter.

The other risks seem more mundane. A COVID-19-induced recession could slow the company’s expansion plans. But as I already mentioned, the current downturn has yet to impact P&G’s profitability.

Management even raised their earnings guidance for full year 2021. People, after all, still need to wash their skin, clean their hair, and brush their teeth no matter how the economy is doing.

Foreign currency swings can also impact results. P&G earns a large chunk of its profits overseas. So, if the U.S. dollar rises, the value of these international earnings declines. That said, these fluctuations tend to even out over time. And, for those with an investment timeframe of over years and decades, they don’t tend to matter.

The bottom line: there is no sure thing in investing. But, thanks to a collection of timeless products, incredible brand recognition, and an exceptional track record, P&G should keep delivering outsized returns (and dividends) through good times and bad.

That’s the power of owning a “Forever Asset.”