Why Institutions Love OMF Stock

There’s a lot to love about OneMain Holdings stock.

The high-interest-rate environment has hurt lenders, as borrowers are less inclined to assume new debt or refinance existing debt.

And, depending on what you believe, interest rates will likely start to fall later this year, extending into 2025 and 2026. Reduced interest rates should encourage the American consumer to buy durable good items, unless the jobs market tanks.

To play what I believe will be a more conducive macro environment for lenders, consider OneMain Holdings Inc (NYSE:OMF).

What’s interesting is the company’s focus on the nonprime consumer. This is the group that is classified as between the low-end credit score subprime borrower and the top-rated prime borrowers. Given the current high-rate climate, I expect opportunities for growth in OneMain’s target market.

Founded in 1912, OneMain Holdings operates 1,300 locations across 44 states, in addition to having an online presence. Its products include personal loans, credit cards, insurance, and mortgage payment solutions. (Source: “About Us,” OneMain Holdings Inc, last accessed July 2, 2024.)

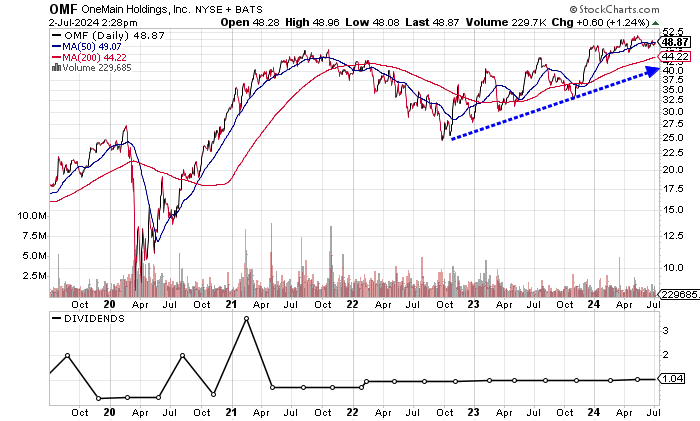

The chart shows OneMain Holdings stock hovering above its 200-day moving average (MA) of $45.50 and just below its 50-day MA of $49.34. The existing trend is positive.

Should OneMain Holdings stock reclaim its 50-day MA, we could see a rally in the shares. Moreover, OMF stock is currently trading in a golden cross, which is a bullish technical crossover when the 50-day MA is above the 200-day MA.

Chart courtesy of StockCharts.

A Free Cash Flow Machine

OneMain Holdings Inc generates significant revenues; there’s been growth in the last three consecutive years up to the period high in 2023.

| Fiscal Year | Revenues (Billions) | Growth |

| 2020 | $3.91 | N/A |

| 2021 | $4.04 | 3.3% |

| 2022 | $4.20 | 4.0% |

| 2023 | $4.28 | 1.9% |

(Source: “OneMain Holdings, Inc. (OMF),” Yahoo! Finance, last accessed July 2, 2024.)

In the first quarter of 2024, OneMain reported revenues of $1.4 billion, up seven percent year over year. The company loaned $2.5 billion in the quarter, which was down 10% versus the first quarter of 2023. This was expected given the high-rate climate, but it should improve as interest rates begin to ratchet lower. (Source: “OneMain Holdings, Inc. Reports First Quarter 2024 Results,” OneMain Holdings Inc, April 30, 2024.)

On the bottom line, OneMain Holdings Inc has consistently delivered generally accepted accounting principles (GAAP) profitability. The results are down from the high in 2021, but the situation is expected to improve over time as rates fall.

| Fiscal Year | GAAP-Diluted EPS | Growth |

| 2020 | $5.41 | N/A |

| 2021 | $9.88 | 82.6% |

| 2022 | $7.01 | -29.0% |

| 2023 | $5.32 | -24.1% |

(Source: Yahoo! Finance, op. cit.)

On an adjusted basis, OneMain earned $5.43 per diluted share in 2023. Analysts expect the company to increase its adjusted earnings to $5.56 per diluted share in 2024, followed by $7.54 to as high as $8.03 per diluted share in 2025. (Source: Yahoo! Finance, op. cit.)

Flipping over to the fund’s statement, we can see that OneMain is a free cash flow (FCF) machine. Its FCF has been used for dividends and share buybacks.

| Fiscal Year | FCF (Billions) | Growth |

| 2020 | $2.21 | N/A |

| 2021 | $2.25 | 1.8% |

| 2022 | $2.39 | 6.2% |

| 2023 | $2.52 | 5.4% |

(Source: Yahoo! Finance, op. cit.)

The balance sheet is debt-heavy, with the company carrying $19.5 billion in total debt and $831.0 million in cash. I don’t see any immediate issues with the debt obligations at this time given the strong profitability and FCF. (Source: Yahoo! Finance, op. cit.)

The Piotroski score, an indicator of a company’s balance sheet, profitability, and operational efficiency, shows a manageable reading of 4.0 for OneMain, which is just below the midpoint of the 1.0 to 9.0 range.

Dividends Look Safe

The forward dividend yield of 8.62% is attractive, having been recently increased. OneMain raised its quarterly dividend to $1.04 per share versus the previous $1.00 per share.

OneMain Holdings stock’s payout ratio of 77.9% is on the high end, but it should decline as earnings rise. (Source: Yahoo! Finance, op. cit.)

My view is that OneMain Holdings stock’s dividend is safe given the strong dividend coverage ratio of 6.1 times.

| Metric | Value |

| Dividend Growth Streak | 1 year |

| Dividend Streak | 6 years |

| 10-Year Average Dividend Yield | 6.8% |

| Dividend Coverage Ratio | 6.1X |

The Lowdown on OneMain Stock

As I mentioned, OneMain Holdings stock is heavily invested in by institutions to the tune of 467 institutions holding an 88.9% stake. (Source: Yahoo! Finance, op. cit.)

Insiders have also been actively buying. Over the last six months, insiders added a net 78,123 shares of OMF stock. (Source: Yahoo! Finance, op. cit.)

In my view, OneMain Holdings Inc should begin to see improvements in its results as interest rates decline.

For income investors, OMF stock provides a nice dividend and price appreciation potential.