Why OPI Stock Has Huge Potential

The outlook for real estate investment trusts (REITs) like Office Properties Income Trust (NASDAQ:OPI) has recently taken a bullish turn.

Since March 2022, the Federal Reserve has raised interest rates 11 times. That was bad for REITs because higher interest rates make it more expensive to borrow capital and service debt. It also weighs down REITs’ profitability.

On the plus side, higher inflation increases property values, although that’s not something investors can really sink their teeth into. What investors have come to appreciate, however, is the Fed taking a pause in its interest rate hikes. That’s what it did in early November, and it’s expected to continue doing that.

With the U.S. expected to avoid a recession, investors are optimistic that the Fed will actually begin cutting interest rates in the spring of 2024. This has been helping juice REIT stocks. Office Properties Income Trust is no exception.

Office Properties Income Trust used to be called Government Properties Income Trust, so that should give you a good idea as to who its biggest tenants are.

Aside from various government agencies, its tenants are companies that operate in sectors including communications, energy services, finance, food, hospitality, law, life sciences, manufacturing, real estate, technology, and transportation. (Source: “Third Quarter 2023 Financial Results and Supplemental Information,” Office Properties Income Trust, October 30, 2023.)

Office Properties Income Trust’s tenant base is focused on sectors with favorable economic and long-term demand outlooks. As of September 30, about 64% of its revenues were from investment-grade tenants.

| Top 10 Tenants | Portion of Annualized Rental Income |

| U.S. Government | 20.0% |

| Alphabet Inc | 4.2% |

| Shook, Hardy & Bacon L.L.P. | 3.6% |

| Bank of America Corp | 3.4% |

| IG Investments Holdings LLC | 3.3% |

| State of California | 3.0% |

| Tyson Foods Inc | 2.3% |

| Northrop Grumman Corp | 2.0% |

| Sonesta International Hotels Corporation | 2.0% |

| CommScope Holding Company Inc | 1.8% |

(Source: Ibid.)

The trust currently owns and leases 154 properties, comprising about 20.7 million square feet in 30 states and Washington, D.C. The company’s occupancy rate of 93.3% has been outperforming the broader market.

Third-Quarter FFO Exceeded Guidance

For the third quarter ended September 30, Office Properties Income Trust reported a net loss of $19.6 million, or $0.41 per share. This compares to third-quarter 2022 net income of $16.9 million, or $0.35 per share. (Source: Ibid.)

The REIT’s normalized funds from operations (FFO) in the third quarter were $49.4 million, or $1.02 per share, compared to $53.8 million, or $1.11 per diluted share, in the same period of last year. That beat the high end of the company’s guidance range.

Its cash available for distribution in the quarter was $17.3 million, or $0.36 per share, versus $28.0 million, or $0.58 per share, in the third quarter of 2022.

Office Properties Income Trust ended the third quarter of 2023 with cash and cash equivalents of $24.3 million. It also had $550.0 million available to borrow under a revolving credit facility, for total liquidity of $574.3 million.

Leasing across the company’s portfolio remains active, with 586,000 square feet of new and renewal leasing in the third quarter, resulting in a total of more than 1.5 million square feet as of September 30.

During the third quarter, the company sold one property for $10.5 million. Since the end of the third quarter, it has entered into agreements to sell two other properties for an aggregate price of $21.3 million.

Commenting on the results, Christopher Bilotto, the president and CEO of Office Properties Income Trust, said, “During the third quarter, OPI continued to advance its business strategies while navigating challenging market conditions facing the commercial office market.” (Source: Ibid.)

He added, “We closed on two mortgage loans for proceeds of $69 million, bringing our total mortgage proceeds this year to more than $177 million. We believe these transactions illustrate the financing opportunities available within our diversified portfolio.”

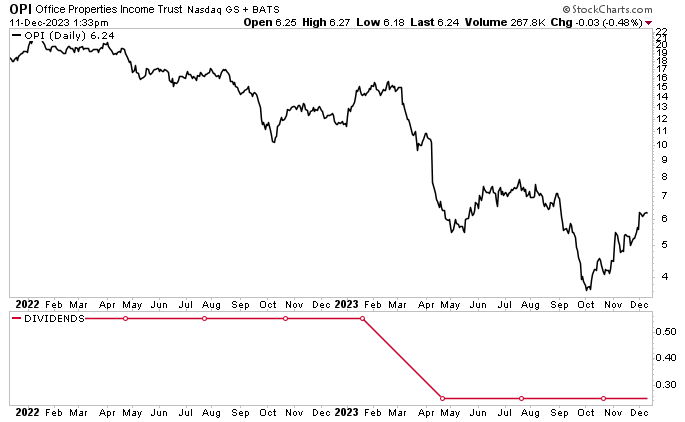

Office Properties Income Trust Stock’s Quarterly Payout Maintained at $0.25 Per Share

For the third quarter, Office Properties Income Trust’s board declared a cash distribution of $0.25, for a yield of 20.73% (as of this writing). Its cash available for distribution of $0.36 safely covered that payout.

While OPI stock has reliably paid dividends every quarter since going public in 2009, management has raised and lowered the payouts at various times. More often than not, however, the company has raised its dividends instead of lowering them.

The trust last raised its payout in 2019, and it reduced its payout in May 2023 (from $0.55 to $0.25).

That dividend cut came around the time the company announced plans to merge with Diversified Healthcare Trust (NASDAQ:DHC). (Source: “Office Properties Income Trust and Diversified Healthcare Trust Announce Agreement to Merge in All-Share Transaction,” Office Properties Income Trust, April 11, 2023.)

Reducing its dividend was expected to increase the company’s financial flexibility during the merger, but in September, management announced that the merger agreement had been terminated. (Source: “Diversified Healthcare Trust And Office Properties Income Trust Mutually Agree to Terminate Merger Agreement,” Office Properties Income Trust, September 1, 2023.)

Hopefully, with the cancelled merger in the rearview mirror, Office Properties will start raising its quarterly payouts again.

The reliable payouts can help provide dividend hogs with a safety net and help them ride out the ongoing stock market volatility.

While it’s been a rough ride for the office REIT industry in general lately, the price of Office Properties Income Trust stock has begun to rebound. As of this writing, OPI stock is down by 45% year-to-date, but it’s up by 30% over the last month and 11% over the last three months.

Chart courtesy of StockCharts.com

Wall Street analysts are increasingly bullish on Office Properties Income Trust stock, with an average 12-month share-price estimate of $12.00, a median estimate of $14.00, and a high estimate of $17.00. This points to potential gains of 92%, 124%, or 172%, respectively.

The Lowdown on Office Properties Income Trust

Investors punished REIT stocks during the COVID-19 pandemic—and since the Fed started raising interest rates—because they thought REITs’ tenants wouldn’t be able to pay their rents, which would cut into the REITs’ profitability.

Thanks to Office Properties Income Trust’s rock-solid tenant base, it was able to weather the pandemic and the interest rate increases better than most.

As mentioned earlier, 64% of the trust’s revenues have been from investment-grade tenants and 20% of its annualized rental income has been from the U.S. government. Moreover, REITs are able to offset inflationary pressure through rent escalations that are built in to their leases.

All this has allowed Office Properties Income Trust to maintain reliable cash flow and provide OPI stockholders with ultra-high-yield dividends.