This Overlooked Stock Could Be an Income Opportunity

If you’re a value investor who’s looking for deals in today’s stock market, chances are you’ll get disappointed pretty quickly. With a bull run that seems unstoppable, the vast majority of stocks on the market are trading at substantially higher valuations than before. In fact, even stocks from “boring” sectors like consumer staples have gotten more expensive because of the sector’s resilience during the COVID-19 pandemic.

To give you an idea, the Consumer Staples Select Sector SPDR Fund (NYSEARCA:XLP)—an exchange-traded fund that tracks the performance of consumer staples stocks in the S&P 500 index—has gone up about 30% over the past five years and now has a price-to-earnings (P/E) ratio of over 20 times. (Source: “The Consumer Staples Select Sector SPDR Fund,” State Street Corporation, last accessed February 17, 2021.)

For investors who already own shares of the consumer staples ETF, that’s not really something to worry about. But if you’re just getting started in building an income portfolio, things certainly don’t look cheap.

And that, dear reader, is why Kellogg Company (NYSE:K) deserves special attention right now.

Headquartered in Battle Creek, MI, Kellogg is a multinational food manufacturing company. It generates most of its sales from snacks and convenience foods like cereal, frozen foods, and noodles. Started as the Battle Creek Toasted Corn Flake Company in 1906, Kellogg now has a portfolio of well-known brands such as “Cheez-It,” “Pop-Tarts,” “Kellogg’s Corn Flakes,” “Rice Krispies,” and “Pringles,” just to name a few.

Now, we know that food producers have generally done pretty well over the last year. In fact, when the pandemic started, some consumers were stocking up on packaged foods, so Kellogg Company’s business actually got a boost.

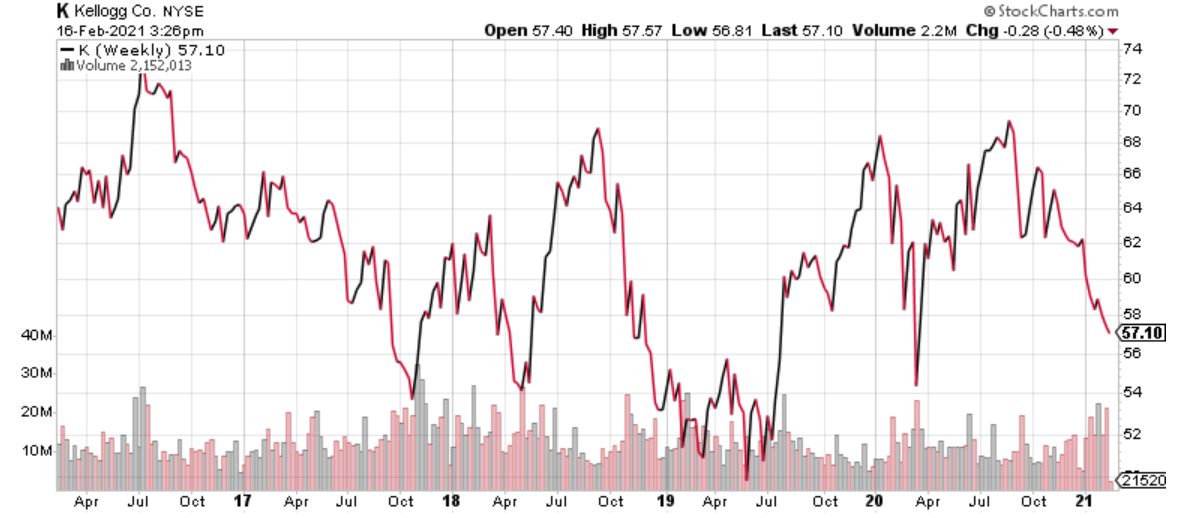

But you wouldn’t know that just by looking at the Kellogg stock chart. Over the last 12 months, K stock tumbled 14.9%. In the past five years, the company’s shares fell 24.4%.

Kellogg Company (NYSE:K) Stock Chart

Chart courtesy of StockCharts.com

One consequence of the sluggish stock price performance is that Kellogg Company now has a P/E ratio of just over 15 times, which is quite a bit lower than the consumer staples sector’s average I mentioned earlier. And keep in mind that the consumer staples sector is not really an expensive one in this bloated market: for the broader S&P 500, the average P/E multiple is about 40 times. (Source: “S&P 500 PE Ratio,” multpl.com, last accessed February 17, 2021.)

And because there’s an inverse relationship between a company’s dividend yield and stock price, Kellogg stock’s tumble has boosted its appeal to income investors. With a quarterly dividend rate of $0.57 per share and a share price of about $57.10, K stock offers an annual dividend yield of four percent.

Again, this is quite a bit better than what’s being offered by its peers and the overall market: the Consumer Staples Select Sector SPDR Fund currently yields 2.6% while the average S&P 500 company yields just 1.5%. (Source: “S&P 500 Dividend Yield,” multpl.com, last accessed February 17, 2021.)

Of course, beaten-down, high-yield stocks are not really known for their dividend safety. But here’s the thing: even though Kellogg stock has not been a hot commodity lately, the company’s dividends remain solid.

Just take a look at Kellogg’s latest earnings report and you’ll see what I mean. In 2020, the company generated $13.8 billion in net sales, representing a 1.4% increase year-over-year. Excluding the impact of acquisitions, divestitures, foreign currency, and differences in shipping days including the 53rd week, the company’s organic net sales rose six percent in 2020. (Source: “Kellogg Company Reports Strong 2020 Results and Issues 2021 Financial Guidance,” Kellogg Company, February 11, 2021.)

At the bottom line, Kellogg earned adjusted net income of $3.99 per share in 2020, up 1.3% from the $3.94 per share it earned in 2019. Considering the company paid four quarterly dividends totaling $2.28 per share last year, the adjusted profits covered the payout with ease.

Looking ahead, management expects Kellogg’s organic net sales to decrease by approximately one percent in full-year 2021. Adjusted earnings per share, on the other hand, are projected to rise by about one percent on a currency-neutral basis for the year. While these numbers are not really exciting, the company’s durable business should have no problem supporting its dividend policy.

In fact, Kellogg Company could end up mailing out bigger dividend checks in the near future.

In the company’s latest earnings conference call, Kellogg’s chief financial officer, Amit Banati, said, “We’ve improved our ability to convert income into cash flow and we deleveraged our balance sheet for increased financial flexibility.”(Source: “Kellogg Company (K) CEO Steve Cahillane on Q4 2020 Results – Earnings Call Transcript,” Seeking Alpha, February 11, 2021.)

Banati continued, “The combination of this improved business condition and enhanced financial flexibility enabled us to review share repurchases this year, after having refrained from them since quarter 1, 2019. In addition, we are increasing our quarterly dividend rate starting in quarter two. This means returning more cash to share owners and it reflects our confidence in the business.”

Bottom Line on Kellogg Company

To sum up, Kellogg is a solid company trading at bargain-like valuations in today’s market. K stock’s four-percent yield deserves the attention of income investors.

And with a dividend hike in the works, investors who pick up Kellogg stock right now could expect to earn higher yield on cost going forward.